Everything these days seems to be automated from reminders for doctors’ appointments, to bill paying, to (something clever). And why not?! Automation is the future, but does this apply to retirement planning as well? Auto-features are gaining traction and participants are more open to them than originally expected. A 2016 survey by American Century found that 70% of participants were:

- in favor of automatic enrollment

- showed interest in regular, incremental automatic increases

- support plan investment re-enrollment into target-date solutions.[1]

Automatic features may help ease plan sponsor woes such as poor participation and low deferral rates.

POOR PARTICIPATION

Left to our own devices Americans are not the most diligent savers. When you consider retirement savings, the outlook is even more bleak. Although 8 out of 10 full time employees have access to an employer-sponsored plan, only 64% participate.[2] To help increase enrollment more and more companies are adopting auto-enroll. This plan design feature enrolls eligible employees into the retirement plan by default, participants are then given the chance to opt out. Auto-enrollment has shown to increase participation from 42% to 91%.[3]

A NEW WAY

The traditional 3% deferral rate is not quite cutting it these days —in fact, 30.2% of companies adopted a 6% or higher default deferral rate by the end of 2015.[4] Employers and participants alike seem to acknowledge that low deferral rates will not provide enough savings to make their retirement aspirations a reality.

DEFERRALS RISING

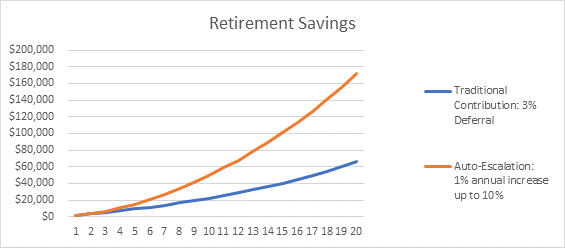

Struggling to help your participants save more? Auto-escalation could help. This plan design feature may help employees overcome inertia by automatically increasing their 401k contribution at regular intervals, typically 1% a year, until it reaches a preset maximum (typically 10%). One percent may not seem like a lot, but together with compound interest, when the time comes to retire, it can make a huge difference! The graph shows how even 1% can affect your nest egg. In the hypothetical example shown below, at the end of 20 years of saving, a participant contributing at 3% would have $65,800 whereas the participant utilizing auto-escalation would have $171,700.[5] That’s over $105,000 difference! Which do you believe would better poise your employees to retire?

TIME FOR ACTION

Employer hesitancy toward adopting auto features is understandable, however, not implementing these advanced features could be short-sighted. Automatic enrollment paired with auto-escalation can help more employees increase their savings and help them achieve their retirement goals. If you have been reluctant to explore these options in the past, maybe it is time to revisit the conversation; after all, the point of offering a company sponsored retirement plan is to help your employees retire successfully.

[1] American Century Investments. “Fourth Annual Plan Participant Study Results.” August 2016.

[2] Bureau of Labor Statistics. “Employee Benefits in the United States.” March 2015.

[3] ASPPA Net Staff. “More Jump on Auto Enrollment Bandwagon, but Not Everyone.” January 2015.

[4] T.Rowe Price. “Reference Point Annual Survey.” April 2016.

[5] Based on Annual salary of $50,000 and 7% return. Deferral rate of 3% vs. 3% starting 1% annual increase up to 10%.

This information was developed as a general guide to educate plan sponsors and is not intended as authoritative guidance or tax/legal advice. Each plan has unique requirements and you should consult your attorney or tax advisor for guidance on your specific situation.